The Corporate Sustainability Reporting Directive (CSRD) sets the standard by which thousands of companies, both in the EU and beyond, will have to report on the social and environmental impacts of their operations and value chain.

CSRD: Prepare for Sustainability Reporting

CSRD 2.0

The European Union adopted the NFRD in 2014, to bring more transparency to material sustainability issues. However, it was criticized for being too lax and limited in scope, as it only covered large public interest companies. That ultimately led the EU to introduce the CSRD, which replaces the NFRD and requires a more detailed approach to sustainability disclosure.

What emerged as a pivotal framework setting a new benchmark for how nearly 50,000 companies are required to account for their environmental and social impact across their operations and value chains, is now being adapted due to the shifting bloc strategy. In a recent development, the European Commission introduced the Omnibus Simplification Package aimed at streamlining certain aspects of the CSRD, offering clarity and potentially alleviating some of the complexities associated with the directive, thus impacting the reporting obligations for many companies. This paper explores the implications of these changes and highlights how EcoVadis can empower your organization to achieve accurate and comprehensive sustainability reporting.

Omnibus-Proposed Changes

The Omnibus package includes a proposal to raise the threshold for mandatory sustainability reporting from 250 to 1,000 employees. If adopted, this change would exempt approximately 80% of companies that currently fall under the CSRD.

With the green light for the “stop-the-clock” directive , the reporting requirements for the wave 2 and wave 3 companies are delayed by two years. EU member states have until the end of 2025 to transpose the “stop the clock” into national laws.

The potential introduction of a “value chain cap” could limit the information that larger, in-scope companies can request from businesses with fewer than 1,000 employees to what is specified in the VSME, the voluntary standard for SMEs.

The European Commission plans to revise and simplify the existing standards through a delagated act, which will be applied to companies required to report in 2028 and 2029. Also, the requirement for sector-specific standards could be removed. The European Financial Reporting Advisory Group (EFRAG), originally in charge of developing the ESRS, was already tasked with providing technical advice on reducing the number of data points, clarifying confusing provisions, and improving compatibility with other laws.

The proposal eliminates the obligation to move from limited assurance to reasonable assurance over time. This change is driven by concerns about the increased costs associated with more demanding reasonable assurance standard, requiring from an auditor a deeper understanding of internal processes and controls.

Who’s in Scope?

CSRD compliance is phased-in. Reporting for wave 2 and wave 3 companies is delayed to 2028-2029.

2024

and reporting in 2025

Entities previously mandated to comply with the NFRD (including public-interest entities and listed companies with 500+ employees). These continue to report according to the CSRD as originally planned.

2-year delay as agreed through the “stop-theclock” directive.

2027

and reporting in 2028

Entities with 250+ employees and net turnover €50 million+ or €25 million+ balance sheet that previously needed to report in 2026. The Omnibus includes a proposal to raise the employee threshold to 1,000.

2028

and reporting in 2029

Listed SMEs that previously needed to report in 2027 and non-EU parent and group companies with €150 million+ net turnover (Omnibus updates may change the applicability thresholds for this wave).

Double Materiality & ESRS

Double Materiality Analysis

This is a key requirement under the ESRS and serves as a foundation for the annual CSRD report.

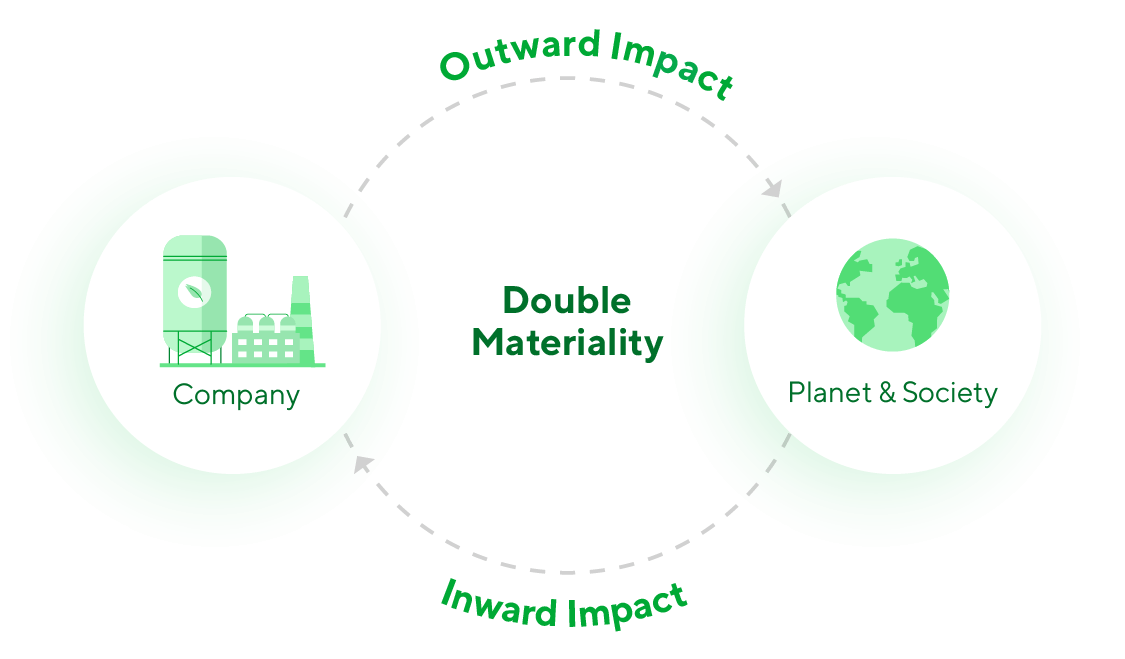

While the Omnibus package aims to streamline certain aspects of the CSRD, the fundamental principle of double materiality remains central to its reporting requirements. This concept dictates that companies must report on sustainability matters from two perspectives: financial materiality (or “outside-in”) and impact materiality (or “inside-out”).

Understanding and correctly applying the principle of double materiality is crucial for effective CSRD reporting. It ensures that companies not only disclose information relevant to their financial stakeholders but also account for their broader societal and environmental responsibilities. This assessment forms the bedrock upon which the entire sustainability report is built, guiding the selection of relevant ESRS and the depth of the required disclosures.

Double Materiality: Two Dimensions

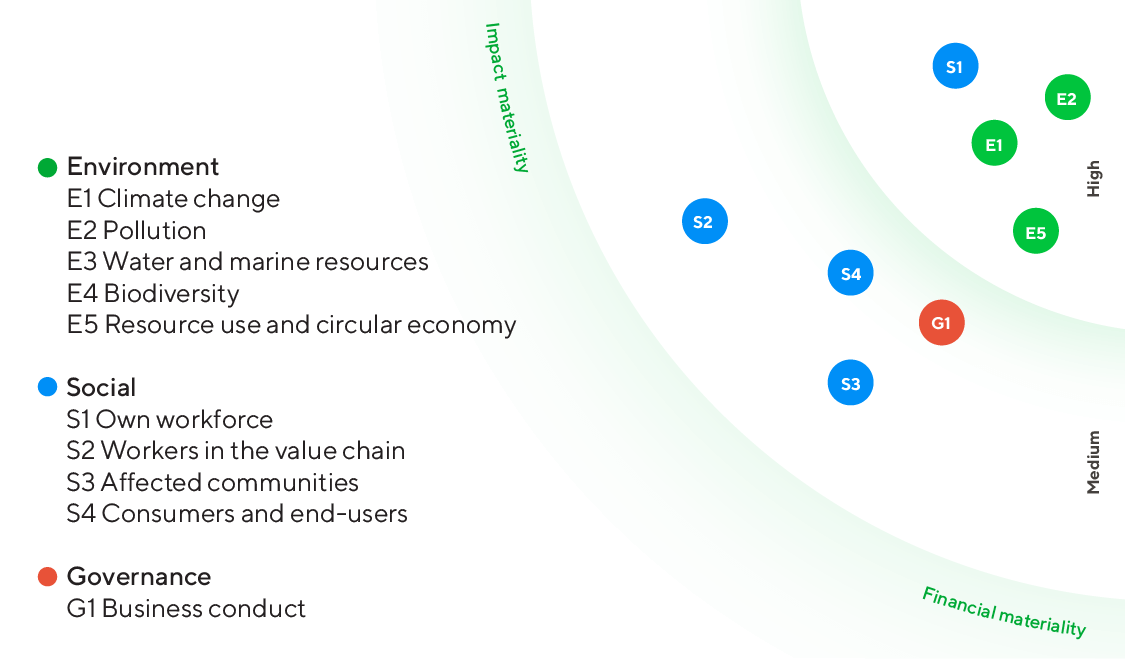

The materiality matrix to the right shows how different E, S and G factors (as outlined in the associated ESRS) can be assessed against two dimensions: financial and impact materiality. The position on the horizontal axis is determined by how much a sustainability-related factor can affect a company financially. The position on the vertical axis is determined by estimating a company’s actual or potential impacts on people or the environment.

Information on sustainability meets the double materiality criteria if it’s material from an impact perspective, a financial perspective, or both.

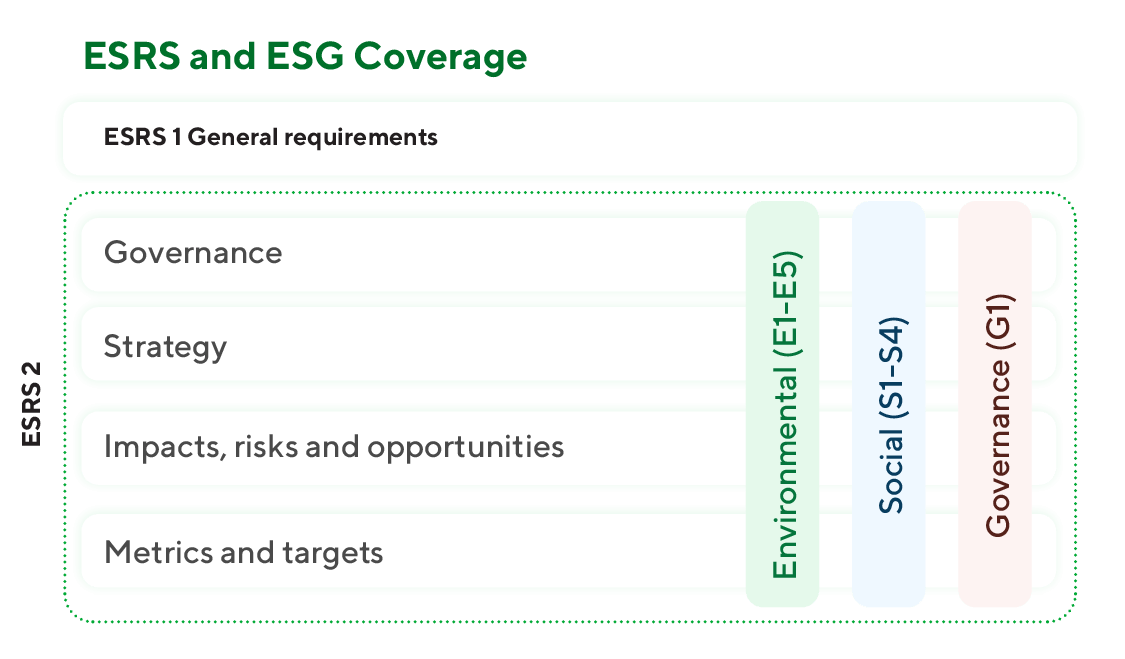

ESRS Explained

The CSRD sets out which companies need to report sustainability-related information and when, while the ESRS support this with detailed disclosure requirements.

The first set of 12 standards includes two cross-cutting and ten topical standards. The Omnibus Simplification Package has direct implications for ESRS: The European Commission has explicitly stated its intention to revise the first set of standards to simplify the reporting requirements.

Mandatory Versus Material Information

Under the first set of ESRS, only ESRS 2 on general disclosures includes mandatory reporting requirements. Aside from ESRS 1, which does not detail specific content but provides general reporting concepts, the 10 topical standards (E1-E5, S1-S4 and G1) are subject to the double materiality assessment.

Companies can decide to omit data for some standards if they can justify that related impacts are not material to their activities. Thus, materiality assessment is the specified tool for narrowing down the reporting content.

Sustainability Risk Mapping

Without a thorough risk mapping exercise, companies will struggle to identify their material topics and fulfill their reporting obligations effectively.

Sustainability risk mapping is the essential first step in the journey towards CSRD compliance. It provides the necessary insights to understand a company’s most significant IROs, informs the due diligence process, guides the scope and prioritization of reporting, facilitates value chain engagement, and ultimately ensures that the resulting CSRD report is meaningful, accurate, and compliant with the ESRS requirements.

The information gathered through risk mapping directly informs the disclosures required under various ESRS, particularly those related to due diligence processes (like ESRS 2) and the management of specific sustainability risks and impacts (as required by the topical standards).

This process helps companies prioritize their reporting efforts by focusing on the areas where their most significant IROs lie. This allows organizations to allocate resources effectively and develop a phased approach to CSRD implementation, starting with the most material topics identified through the risk mapping.

Effective risk mapping extends beyond a company’s direct operations to encompass its value chain. This necessitates understanding the IROs associated with suppliers and other chain actors. This process highlights areas where stakeholder engagement is crucial for data collection, risk mitigation, and ultimately, accurate and comprehensive CSRD reporting.

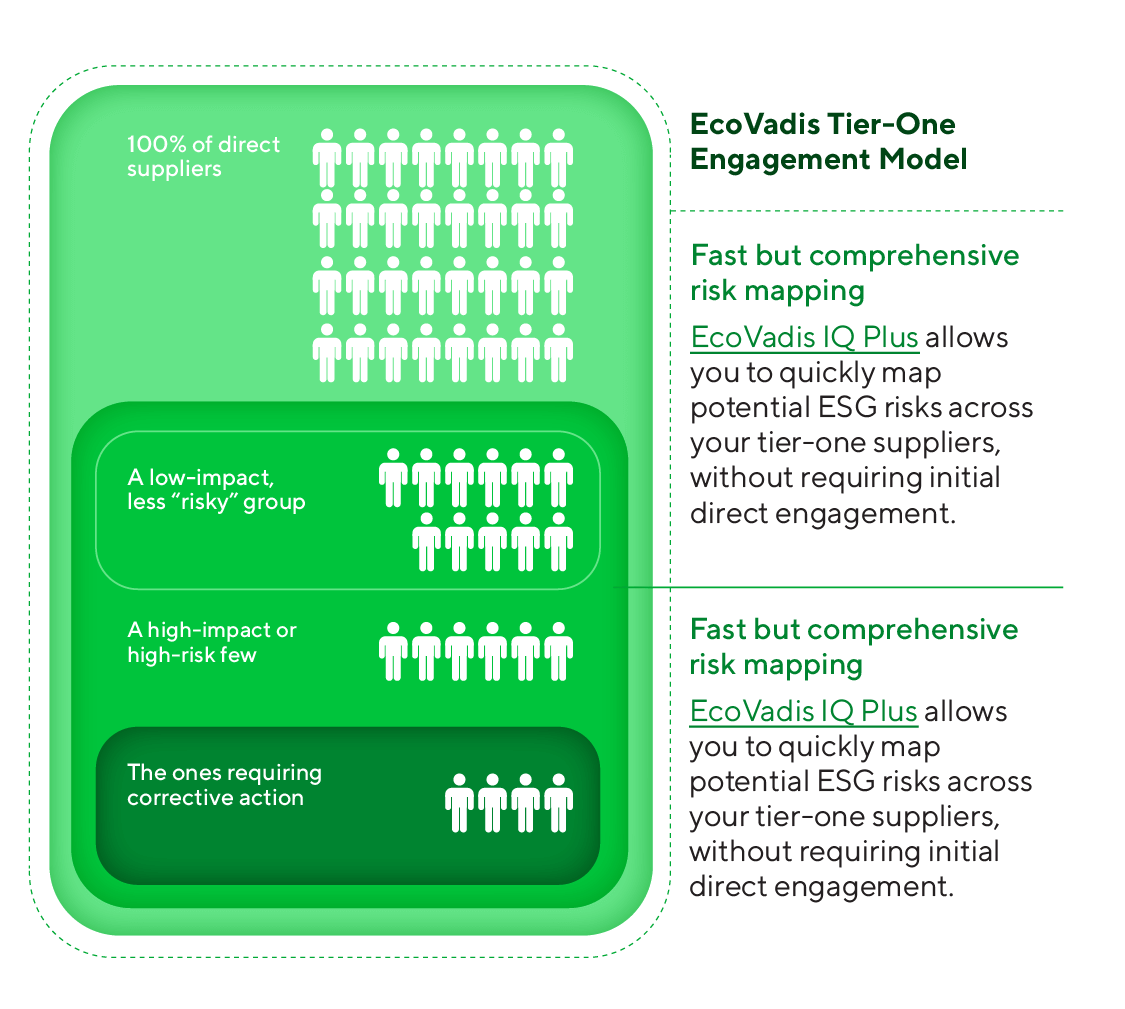

Phased and Prioritized Approach

While the scope of analysis and reporting is not limited to tier-one business relationships, focusing on direct suppliers first offers several significant benefits for CSRD implementation. Starting here creates a more manageable scope for initial data collection and analysis compared to immediately tackling the entire, often complex, multi-tiered supply chain. Also, you have the most leverage and influence over your direct suppliers to request and potentially mandate changes in their sustainability practices and data provision.

Early Days of Reporting

In a three-year window, companies will have to bring their sustainability reporting up to the same standard as financial reporting.

The expectation is that sustainability data and reports will get better. Estimates and sector-average data will initially be allowed if collecting primary data proves challenging.

Ready to get started?