Corporate sustainability has entered its execution phase. Delay now carries financial, regulatory, and operational costs. For business leaders, 2026 is no longer about debating distant commitments, but about managing the physical realities of climate risk and the “reporting divide” that is emerging in a fragmented regulatory landscape.

From Net-Zero Narratives to Climate Reality

While the backdrop of the Amazon rainforest at COP30 reminded the world of the physical urgency of climate risk, a more pragmatic revolution is taking hold in the corporate sector. The consensus for 2026 is clear: companies are prioritizing practical action and measurable impact over broad, long-term alignment.

With the 1.5°C threshold effectively out of reach, companies are being forced to confront a harder truth: strategy must now work in a destabilized climate, not a theoretical one. Major institutions are transitioning from rigid membership commitments – such as the Net-Zero Banking Alliance moving to a guidance framework, alongside major energy companies, banks, and retailers softening their previous climate pledges. While this shift does not mean the end of the long-term Paris Agreement temperature goal, as fighting for every fraction of each degree beyond 1.5°C matters, companies are focusing on granular, short-term targets and financial materiality, with political and regulatory headwinds only accelerating this approach.

Dual-track strategies are emerging instead: continued emissions reduction, where it is financially and operationally viable, paired with growing investment in adaptation – climate-proofing assets, suppliers, and value chains against the volatility that is already locked in.

Political Headwinds and Trade-Offs

Political volatility has become a structural business risk. Companies that wait for policy clarity will absorb the cost of delay through disrupted supply, rising tariffs, and stranded assets. While an anti-net-zero stance in the political sphere accelerates a backtrack on some public commitments, the private sector remains laser-focused on economic continuity.

In the US, the primary driver for already-strained businesses in 2026 is navigating economic disruption, with tariffs and trade wars being the most significant external risk, flagged by 72% among 400 companies surveyed for our 2025 US Business Sustainability Outlook. They are making a calculated, pragmatic choice to protect their value chains, foreseeing (56%) potential trade-offs between tariff policies and sustainability priorities, ensuring business continuity remains paramount.

From Climate Exposure to Financial Resilience

While trade dynamics shift, climate adaptation remains a constant financial imperative. The global economy has already absorbed $3.6 trillion in physical climate losses in the past five years. These are no longer tail risks. They are operating conditions.

This resilience strategy is now expanding beyond carbon. Biodiversity loss and water stress are no longer viewed as separate, manageable risks. Following the rapid adoption of the Taskforce on Nature-related Financial Disclosures (TNFD), leading companies are now managing “nature positive” impacts by treating local water basins and ecosystems as a single, critical asset class.

The strategic divide in 2026 is no longer between leaders and laggards. It’s between companies that redesign their supply chains for volatility and those that quietly absorb escalating costs until the margin disappears.

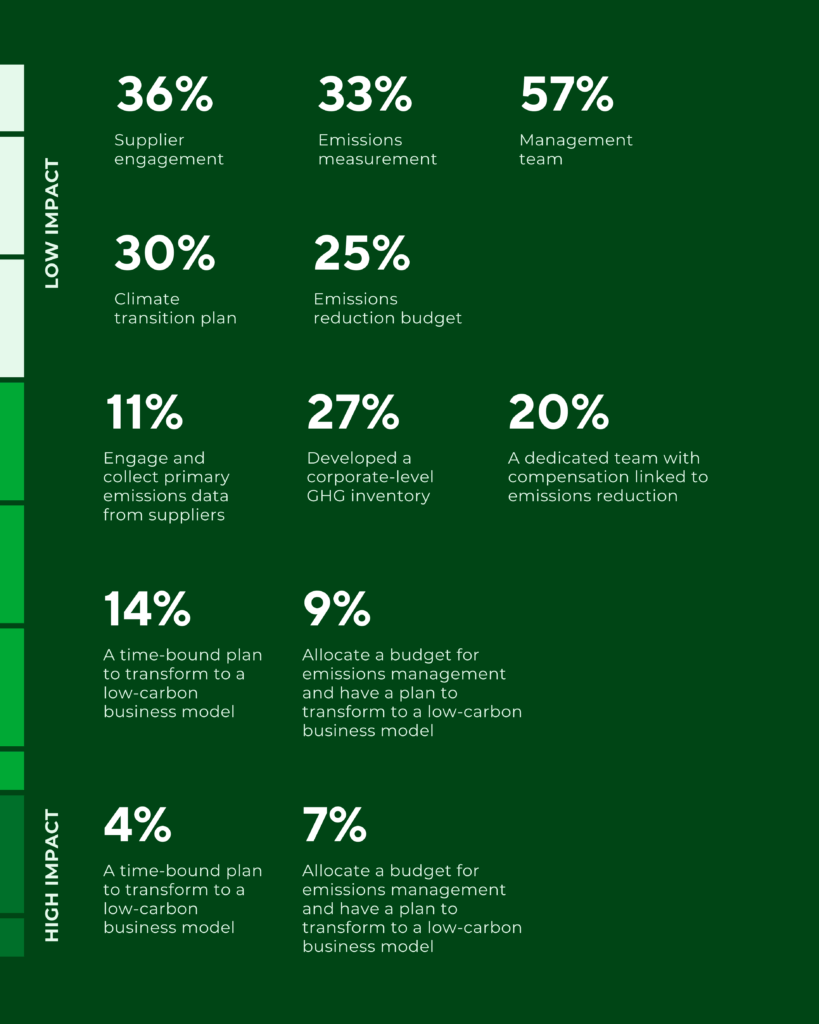

Unlocking Value Through Scope 3 Execution

Our analysis with BCG suggests there are significant opportunities for returns in managing Scope 3 emissions. Several levers of change can help drive this, such as integrating climate criteria into procurement, establishing science-based targets, or fostering technology-driven collaboration. Emissions at the product level also present a promising path: a substantial increase in Scope 3 accuracy, with actual carbon data linked to a product mix, allowing buyers to move from industry averages to detailed emissions tracking.

Companies that actively engage their suppliers are 9x more likely to achieve their Scope 3 targets – yet two-thirds still do not. In 2026, inaction here is no longer a capacity issue. It is a leadership decision.

Adoption of actions that unlock Scope 3 results (EcoVadis-assessed cohort, n=7,659)

Source: EcoVadis x BCG Carbon Action Report

The era of estimation is ending. Product-level data is becoming mandatory, and companies now stand or fall on their ability to scale verifiable compliance. The shift to product-level emissions data allows buyers to move from industry averages to precise, primary data, ultimately enabling smarter procurement decisions. AI is the accelerator here: with 81% of executives already leveraging AI for sustainability, data automation is becoming a strategic asset for performance tracking and risk management.

Standardizing the Demand for Data

A tightening regulatory landscape is addressing the demand for sustainability and emissions data with force.

Mechanisms like the EU Carbon Border Adjustment Mechanism (CBAM), which took full effect as of January 1, 2026, and the Deforestation Regulation (EUDR) are standardizing the demand for data and rewarding transparent supply chains. Simultaneously, mandatory disclosure is going global – from California’s SB 253, mandating Scope 3 data reporting for thousands of companies operating in the state during the 2026 fiscal year, to new standards in Australia, Hong Kong, and Japan, aligning the world around verifiable data.

Regulatory pressure has turned verifiable data into a premium product. Suppliers who cannot produce it will compete on price alone. Those who can will compete on trust. In an era of AI deepfakes and sophisticated greenwashing, trusted and auditable data is becoming a monetizable asset. Buyers can no longer rely on unverified claims or industry averages. Consequently, suppliers who can provide the opposite will command a distinct price premium over their opaque competitors.

For 2026, the competitive edge belongs to those who treat compliance data not as a legal defense, but as a commercial product.

The New Language of Reporting

As we enter 2026, a “reporting divide” is actually helping to clarify corporate priorities. The International Sustainability Standards Board (ISSB) is solidifying a global baseline that treats climate reporting as a core component of financial risk and enterprise value.

This shift empowers companies to speak the language of investors. Adoption of TCFD frameworks in the Americas has increased from 27% in 2022 to 35% in 2025, and climate risk disclosure remains steady in financial filings regardless of political shifts. Meanwhile, broader social topics, such as Diversity, Equity & Inclusion (DEI), are facing political friction.

Conclusion: The Pragmatist’s Advantage

As we look toward 2026, the era of ambiguity is ending. The market is separating into two camps: those distracted by the noise of political debate, and the practitioners who are quietly building the infrastructure to navigate it.

In 2026, waiting for certainty is itself a risk strategy. The winners will be those who act before regulation, disruption, and climate volatility force their hand.

If you want to talk about comprehensive sustainability management that balances both financial risk and holistic ESG requirements, contact EcoVadis.