ChatGPT

ChatGPT  Gemini

Gemini  Perplexity

Perplexity  Claude

Claude  Grok

Grok

![A vertical or circular process graphic illustrating all eight steps as a continuous cycle rather than a linear list. Reinforces the idea that ESG auditing is ongoing.]](https://ecovadis.com/wp-content/uploads/2026/06/eight-step-esg-audit-process-checklist.svg)

Gain insights from 30+ sustainability leaders, including superstars like Paul Polman, former CEO of Unilever, and Helena Helmersson, former CEO of H&M Group. Learn how to build a sustained advantage through responsible business practices.

7th July 2026

Real Progress, Real Gaps: The 10th Edition EcoVadis Sustainability Ratings Index

Read summarized version with:

The share of companies reaching Advanced+ status – scoring 65 or above on the EcoVadis 0-100 rating scale – jumped from 19% to 29% in a single year, the largest single-year gain in ten years of data. Average scores are up across every theme. The Environment theme more than doubled its Advanced+ rate between 2021 and 2025. Sustainable Procurement, historically the weakest area, recorded its biggest one-year gain on record. Companies in several emerging markets are improving at rates that would have looked implausible four years ago.

The supply base is moving. That much is not in question.

But the tenth edition of the EcoVadis Sustainability Ratings Index – drawing on nearly 200,000 scorecards from 100,000+ companies assessed between 2021 and 2025 – tells a more complicated story than the headline numbers suggest. Because movement, it turns out, is not evenly distributed. And in the places that matter most to buyers right now, the gaps remain wide.

The compounding return on engagement

The single clearest pattern in ten years of data is this: companies rated multiple times perform substantially better than those that aren’t.

The evidence is most visible when you isolate the cohort of companies assessed in both 2021 and 2025. Of those companies – the ones that stayed in the network, reassessed, and acted on what a rating cycle revealed – nearly 46% had reached the Advanced or Outstanding level by 2025. That is not the network average. That is what sustained engagement, applied consistently over four years, actually produces.

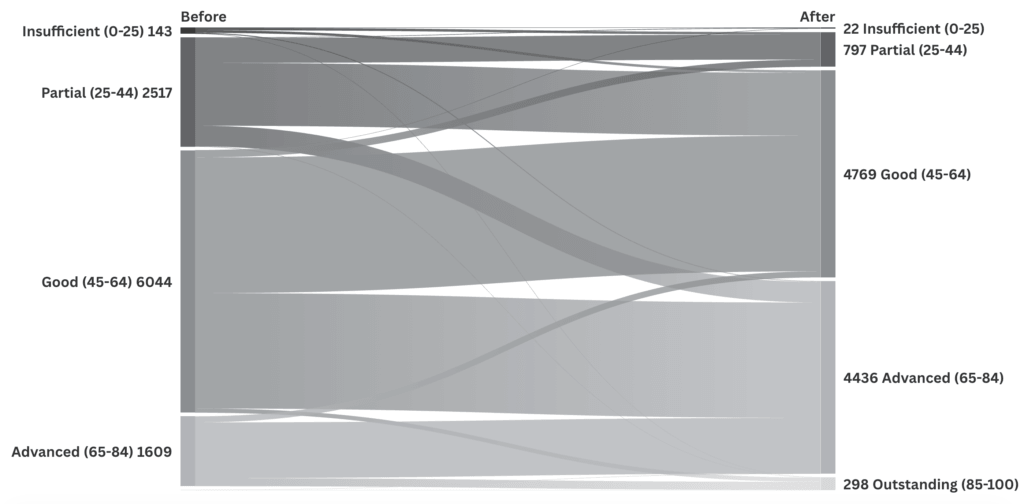

Progression of companies rated in 2021 and again in 2025

In 2021, 59% of that same cohort sat in the Good tier (45–64), and 24% were Partial (25–44). Four years later, the Good tier has shrunk to 46% as companies moved up, the Partial tier has collapsed from 24% to under 8%, and the Advanced tier has grown from 16% to 43%. The Insufficient category – 1% in 2021 – is now virtually gone.

This is what the compounding return on assessment looks like in practice: a structural shift in where a population sits.

First-time rated companies in 2025 average 51.5 overall. Those that have been in the EcoVadis network for ten or more years average 63.2. That 12-point gap – and the 28-point difference in Advanced+ rates between those two groups – is not explained by size, sector, or geography. It is the compounding return of sustained engagement: documentation built over cycles, processes embedded, practices anchored in operational routines, and improved year after year.

For procurement teams managing risk across large supply bases, this divergence is the strategic challenge that the data is surfacing. The supply base is not moving as a single wave. It is separating into a cohort of rapidly improving companies and a much larger group still building the foundations.

Where the gaps are widest

97% of rated companies now have at least a few Labor & Human Rights measures in place. Only 75% report on them. In Ethics, 80% have measures; 38% report. Sustainable Procurement sits at 66% and 36% respectively.

These are not marginal differences. They represent thousands of companies that are doing things they are not documenting, or documenting things they are not making visible. And in a landscape where 68% of buyers have deployed AI in their sustainability programs, the quality of what those systems can produce is only as good as what suppliers are willing to report.

The carbon picture makes this most concrete. 85% of leading buyers are now collecting product-level carbon footprints from their supply chains. 30% of suppliers provide no carbon data at all. Just 19% report Scope 3 upstream emissions; 15% report downstream. Buyers are building infrastructure designed to process data that, for a significant share of the supply base, does not exist yet.

This is not a failure of ambition. Companies are investing in the energy transition – renewable energy procurement, carbon audits, and employee training are all rising in the data. What is missing is the measurement layer that turns operational action into the verified, decision-grade data buyers and regulators need.

What ten years of data shows

When EcoVadis published its first Index, supply chain sustainability was fragmented, voluntary, and largely invisible to procurement teams. The data was thin. The standards were inconsistent.

Ten years later, none of that is true. Sustainability ratings have become strategic infrastructure. Regulatory frameworks have replaced voluntary disclosure as the baseline expectation in major markets. And the conversation has shifted decisively from ambition to execution – not whether companies have sustainability commitments, but whether they can demonstrate, verify, and improve the practices that sit behind them.

The tenth edition arrives at the moment when that shift is most visible in the data, and when the distance between the companies moving fastest and those still building the foundations is widest.

Read the EcoVadis Sustainability Ratings Index, 10th Edition →